[tta_listen_btn listen_text=”Audio” pause_text=”Pause” resume_text=”Resume” replay_text=”Replay”]

Rivalry with China, fallout from Russia’s war in Ukraine and wrangling once again in Washington over the U.S. debt ceiling have put the dollar’s status as the world’s dominant currency under fresh scrutiny.

Russia’s sanctions-imposed exile from global financial systems last year also fuelled speculation that non-U.S. allies would diversify away from dollars.

Below are some arguments why de-dollarisation will happen – or possibly why it won’t.

SLIPPING RESERVE STATUS

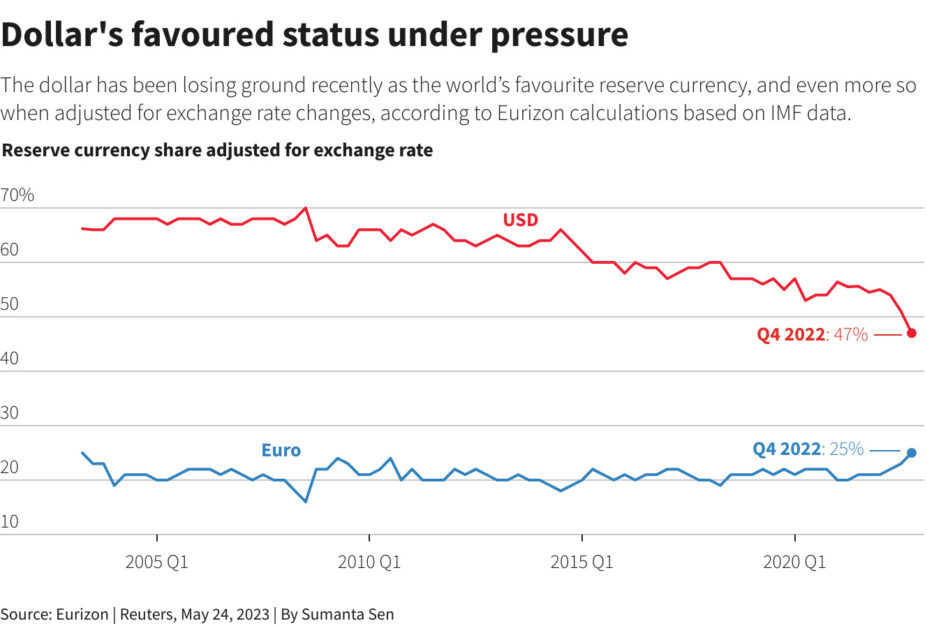

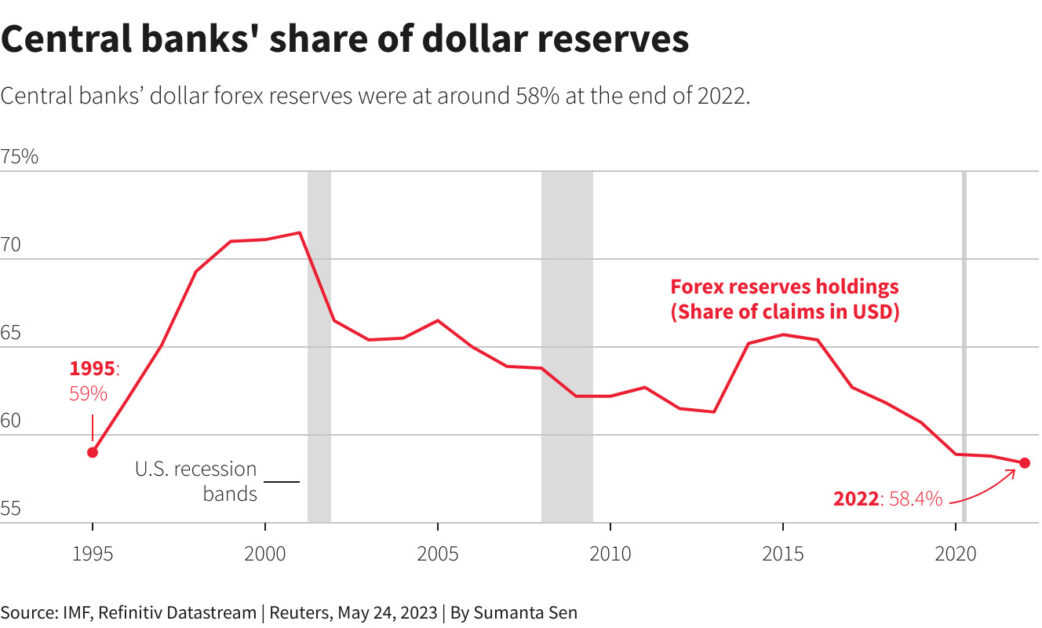

The dollar share of official FX reserves fell to a 20-year low of 58% in the fourth quarter of 2022, according to International Monetary Fund data.

Stephen Jen, CEO of Eurizon SLJ Capital Limited, said that the shift was more pronounced when adjusted for the exchange rate.

“What happened in 2022 was a very sharp plummeting in the dollar share in real terms,” Jen said, adding this was a reaction to the freezing of half of Russia’s $640 billion in gold and FX reserves following its 2022 invasion of Ukraine. This sparked a re-think in countries such as Saudi Arabia, China, India and Turkey about diversifying to other currencies.

TAKING THE LONGER VIEW

The dollar share of central bank’s foreign reserves in the final quarter of 2022 did hit a two-decade low, but the move has been gradual and it is now at almost a similar level as in 1995.

Central banks put rainy-day funds in dollars in case they need to prop up exchange rates during economic crises. If a currency weakens too far against the dollar, oil and other commodities traded in the U.S. currency become expensive, raising living costs and fuelling inflation.

Many currencies, from the Hong Kong dollar to the Panama balboa, are pegged against the dollar for similar reasons.

WANING GRIP ON COMMODITIES

The almighty dollar has had a lock on commodity trading, allowing Washington to hinder market access for producer nations from Russia to Venezuela and Iran.

But trade is shifting. India is purchasing Russian oil in UAE dirham and roubles. China switched to the yuan to buy some $88 billion worth of Russian oil, coal and metals. Chinese national oil company CNOOC and France’s TotalEnergies completed their first yuan-settled LNG trade in March.

After Russia, nations are questioning “What if you fall on the wrong side of sanctions?” said BNY Mellon strategist Geoffrey Yu.

The yuan’s share of global over-the-counter forex transactions rose from almost nothing 15 years ago to 7%, according to the Bank for International Settlements (BIS).

BUT TOO COMPLEX A SYSTEM

De-dollarisation would require a vast and complex network of exporters, importers, currency traders, debt issuers and lenders to independently decide to use other currencies. Unlikely.

The dollar is on one side of almost 90% of global forex transactions, representing about $6.6 trillion in 2022, according to BIS data.

About half of all offshore debt is in dollars, the BIS said, and half of all global trade is invoiced in dollars.

The dollar’s functions “all reinforce each other”, said Berkeley economics and political science professor Barry Eichengreen.

“There just isn’t a mechanism for getting banks and firms and governments all to change their behaviours at the same time.”Reuters Graphics

A FRAGMENTED FUTURE

While there may not be a single-dollar successor, mushrooming alternatives could create a multipolar world.

BNY Mellon’s Yu said nations were realizing that one or two dominant reserve asset blocks was “just not diversified enough.”

Global central banks are looking at a wider variety of assets, including corporate debt, tangible assets such as real estate, and other currencies.

“This is the process that is underway,” said Mark Tinker, managing director of Toscafund Hong Kong. “The dollar is going to be used less in the global system.”

AN UNSHAKEABLE BASIS

Because large bank deposits are not always insured, businesses use government bonds as a cash alternative. The dollar’s status is therefore underpinned by the $23 trillion U.S. Treasury market – viewed as a safe haven for money.

“The depth, liquidity and safety of the Treasury market is a big reason why the dollar is a leading reserve currency,” said Brad Setser, a Council on Foreign Relations fellow who tracks cross-border currency flows.

International holdings of Treasuries are vast and there’s no credible alternative yet. Germany’s bond market is relatively small, at just over $2 trillion.

Commodity producers may agree to trade with China in yuan, but recycling cash into Chinese government bonds remains tricky due to difficulties in opening accounts and regulatory uncertainty.

“But you can hop on an app and trade Treasuries from anywhere,” Natwest Markets emerging markets strategist Galvin Chia said.