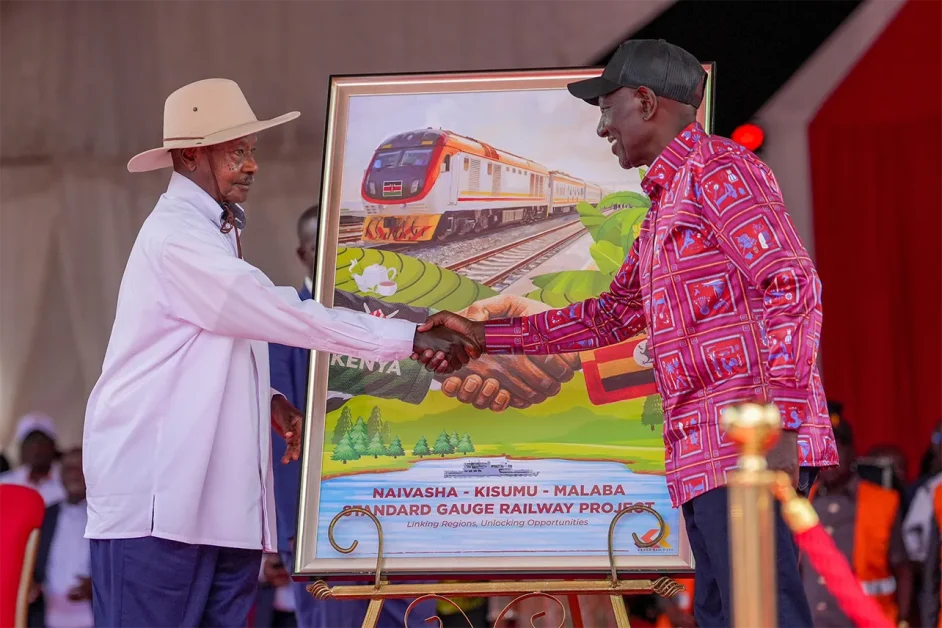

ON Saturday, 21 March, at Kibos in Kisumu County, Kenyan President William Ruto and Ugandan President Yoweri Museveni tightened bolts in the symbolic African tradition of a ground-breaking ceremony for Phase 2C of Kenya’s Standard Gauge Railway – the 107-kilometre Kisumu-Malaba section that will, for the first time, bring the Chinese-built railway to Kenya’s western border with Uganda.

The moment is significant. It completes what Ruto described as “a continuous railway artery of nearly 1,000 kilometres from Mombasa to Malaba” – a line that, once Uganda builds its onward section from Malaba to Kampala, will stitch together two of East Africa’s largest economies by rail for the first time in the modern era.

But the groundbreaking is as much a political milestone as an engineering one. The SGR has become the defining case study of China’s Belt and Road Initiative on the continent – celebrated for ambition, condemned for its debt burden, and now, cautiously, reprieved by necessity.

THE PROJECT: WHAT IS BEING BUILT

Phase 2C, valued at $943 million and to be constructed by China Communications Construction Company (CCCC), covers 107 kilometres from Kisumu to the Malaba border post with Uganda. It follows hot on the heels of Phase 2B – the 264-kilometre Narok–Kisumu section that was ceremonially launched just two days prior, on 19 March, at Motonyi in Narok County.

Together, these phases extend the SGR west from Naivasha – where the line had stalled since 2019 – through the Rift Valley and into Kenya’s agriculturally rich western hinterland, linking maize belts in Narok, tea country in Kericho and Bomet, and the Lake Victoria fish sector in Kisumu to the port of Mombasa. The combined investment across both phases is estimated at around Ksh 500 billion ($3.8 billion).

Once the Kisumu–Malaba section is complete, projected for June 2027, cargo will travel the full Mombasa–Malaba corridor by rail. Transit from Mombasa to Kampala currently averages over 100 hours, much of it on deteriorating roads. The new corridor is projected to cut freight costs by at least 40 percent per tonne per kilometre and reduce transit times by close to 30 percent.

| SGR PHASE 2C — KEY FIGURES | |

| Section | Kisumu to Malaba (Phase 2C) |

| Distance | 107 kilometres |

| Value | $943 million (approx. Ksh 122 billion) |

| Contractor | China Communications Construction Company (CCCC) |

| Target completion | June 2027 |

| Total corridor (Phases 2B + 2C) | ~371 km | ~Ksh 500 billion ($3.8bn) |

| Mombasa–Malaba full corridor | ~1,000 km |

| Projected freight cost reduction | 40% per tonne/km |

| Projected transit time saving | ~30% |

THE DEBT SHADOW: KENYA’S BURDEN WITH BEIJING

The fanfare of Saturday’s ceremony cannot fully obscure the financial distress that has characterised the SGR from its inception. Kenya borrowed approximately $5.08 billion from China’s Export-Import Bank between 2014 and 2015 to finance the first two phases of the SGR, from Mombasa to Nairobi and onward to Naivasha. The SGR is now the largest infrastructure project Kenya has ever undertaken — and its most financially fraught.

According to Kenya’s Auditor-General Nancy Gathungu, Kenya owed its Chinese creditors $741 million in principal, $222 million in interest, and $41 million in penalties in the 2025–2026 fiscal year alone — penalties that she described as “not a proper charge to public funds.” Annual debt service payments to China have consumed more than 81 percent of Kenya’s total foreign debt service in some months. The SGR arrears held by Kenya Railways Corporation stood at Ksh 413.4 billion — approximately $3.2 billion — by June 2025.

A structural peculiarity has compounded the problem: under the original loan agreement, all SGR revenues must be deposited into a joint escrow account managed with Exim Bank, which requires a minimum balance of Ksh 25 billion before any surplus can flow to debt repayment. That threshold has never been met. The result is a perverse arrangement where the SGR earns revenue — it has generated Ksh 112 billion since launch — yet none of those earnings has formally reduced the loan balance.

“These penalties expose the public to expenditures that could otherwise have been avoided. This expenditure is not a proper charge to public funds.”

Kenya Auditor-General Nancy Gathungu, July 2025

Kenya has taken steps to ease the pressure. In October 2025, the National Treasury completed a landmark conversion of the three dollar-denominated Exim Bank SGR loans — totalling a residual $3.5 billion — into Chinese yuan, reducing the interest rate from over 6 percent to approximately 3 percent. The Treasury expects to save around $215 million annually as a result. The SGR repayment period has also been extended to 2040.

Beijing’s leverage is unmistakable: it has withheld fresh credit facilities for the extension precisely because the original loans remained in arrears. The groundbreaking of Phase 2C represents, in part, the culmination of the debt negotiation as much as of the construction planning. China’s policy banks are understood to have conditioned the release of new financing on Kenya’s commitment to complete the border crossing.

MUSEVENI’S VISION: THE DRC CORRIDOR AND BEYOND

Perhaps the most geopolitically significant element of Saturday’s event was the presence and ambition of Ugandan President Yoweri Museveni, who used his address at Kibos to sketch a railway map for the wider region that extends far beyond the Kenya–Uganda border.

Speaking at the ceremony, Museveni outlined Uganda’s complementary railway plans, committing to push the line from Malaba to Kampala, then westward to Kasese and the border town of Mpondwe, linking directly to the Democratic Republic of Congo. He also referenced a northern branch from Tororo through Gulu to Nimule and on to Juba in South Sudan, and a southern line from Bihanga to Kigali in Rwanda.

“We’re going to push our section from Malaba to Kampala, then to Kasese and Mpondwe linking to the DRC. We are also working on the railway from Tororo to Gulu, then Nimule to Juba, as well as the line from Bihanga to Kigali.”

President Yoweri Museveni of Uganda

The DRC linkage is especially significant. The eastern DRC holds some of the world’s most significant mineral deposits — coltan, cobalt, gold, and cassiterite — that are currently transported at enormous cost by road or river. A direct rail connection from Mpondwe through the Kasese corridor to the SGR, and thence to Mombasa, would transform the mineral supply chain for global battery and electronics industries — and significantly alter East Africa’s strategic position in global critical mineral supply chains.

Kenya, Uganda, and Rwanda have already signed an SGR Protocol and Tripartite Agreement to govern the cross-border system. The framework provides the institutional scaffolding for the broader regional vision, though financing and timeline commitments for the Uganda and Rwanda sections remain uncertain.

ECONOMIC LOGIC: THE BUSINESS CASE

For African businesses and investors, the Kisumu–Malaba SGR presents both opportunity and context-dependent risk. The economic logic is compelling: East Africa’s Northern Corridor — the trade route linking Mombasa to landlocked Uganda, Rwanda, Burundi, South Sudan, eastern DRC, and beyond — currently moves the overwhelming majority of its cargo by road, a mode of transport that is expensive, accident-prone, and destructive of road infrastructure.

The SGR has already demonstrated its freight potential. In its eight years of operation on the Mombasa–Nairobi–Naivasha corridor, the railway has carried more than 15 million passengers and 45 million tonnes of freight. Ruto described the agricultural potential vividly: “This railway will connect farmers to markets, enabling the fast and efficient transportation of goods such as livestock, tea, dairy, grains, and fish across the region.”

Museveni was more direct about the strategic intent: “Our plan is to transfer all heavy cargo to the railway — all heavy luggage to be moved from the road to the train. Then transfer all petroleum products to the pipeline.” The shift of petroleum transit from road to pipeline would alone have dramatic consequences for road maintenance costs and road safety across Uganda and Kenya.

Ruto highlighted that the railway would foster “the growth of industrial parks, logistics hubs, and commercial centres along the corridor,” with implications for property development, warehousing, cold-chain logistics, agro-processing, and manufacturing investment in towns that have historically been bypassed by economic development.

RISKS AND UNANSWERED QUESTIONS

The business community will be right to approach the project with clear-eyed caution. Critics of the SGR — including prominent Kenyan entrepreneur Jimi Wanjigi, who described the original loans as “the beginning of a long fraud on Kenyans” — point out that the project has consistently generated revenues below the thresholds required by its own financing structure. The escrow account design has prevented operational revenues from servicing the debt even when they were available.

A structural concern also arises from the budgetary record: Kenya’s own Ministry of Transport has acknowledged that no formal budgetary allocation for the Phase 2B and 2C extensions has been made in the current or next three financial years. The government says the last 40 percent of the line will be built by a consortium of Chinese companies who will charge for use — a public-private structure whose specific terms, revenue-sharing arrangements, and operational governance remain publicly unspecified.

The financing model for Uganda’s onward section is even less clear. Kampala has signalled intent but has not publicly secured financing from either Chinese or multilateral sources for its planned segments. Without Uganda’s section — currently the critical missing link in the regional corridor — the full trade logic of the Mombasa–DRC rail corridor cannot be realised.

On the debt side, Kenya’s public debt stood at approximately 70 percent of GDP by mid-2025, well above the government’s own medium-term target of 55 percent. The restructuring and yuan conversion have provided breathing room, but analysts at Chatham House have cautioned that the SGR’s financial collapse reflects “a planning process driven more by short-term electioneering than strategic need” — a warning equally applicable to successor phases if governance is not substantially strengthened.

THE BROADER AFRICAN CONTEXT

The SGR’s renewed momentum arrives at a moment when the African continent’s appetite for infrastructure development is undiminished, even as its financing options are in flux. China’s development banks, having absorbed losses across Zambia, Ghana, and Sri Lanka, have adopted a more cautious posture — the Kisumu–Malaba phase is in part funded by the CCCC consortium under a commercial model rather than pure sovereign lending, a structural shift worth watching.

For the African Union’s Programme for Infrastructure Development in Africa (PIDA) and its continental free trade agenda under the AfCFTA, the SGR represents a proof of concept that rail-based regional integration is achievable, even if the financial structure has been deeply problematic. The completion of the Mombasa–Malaba corridor, and the potential DRC link, would represent one of the most commercially significant transport infrastructure projects on the continent this decade.

Whether Saturday’s ceremony marks the beginning of a genuine transformation of East Africa’s logistics architecture — or another chapter in a saga of ambition outrunning execution — will depend on factors that no single groundbreaking can determine: the speed of Uganda’s rail construction, the terms of the build-operate agreements, Kenya’s capacity to stabilise its public finances, and above all, whether the freight actually materialises at volumes sufficient to justify the investment.

The railway of the 21st century, as Ruto noted, must do what the colonial railway of the 20th century also did: not merely connect places, but create them. That ambition is real. The question for Africa’s business community is whether the governance will be equal to it.